Cayside Review: 2026 Q1

This newsletter includes our 2026 First Quarter review, global market update and outlook, key numbers, and announcements.

"The most difficult thing is the decision to act; the rest is merely tenacity. The fears are paper tigers. The process is its own reward."

-Amelia Earhart

The first quarter of 2026 delivered a sharp reminder that markets do not move in straight lines. U.S. equity indices declined across the board, with the S&P 500 falling -4.4% as the Iran conflict triggered the largest oil supply disruption since 1979, reignited inflation concerns, and trapped the Federal Reserve between competing mandates. Oil and Gold were among the best-performing asset classes, Bitcoin declined sharply, and international equities demonstrated resilience through February before reversing in March. The investment regime of the prior three years, including indexed, passive concentration in U.S. mega-cap technology, a Fed-as-backstop mentality, and compressing volatility is being meaningfully tested. We believe this transition creates both risk and opportunity, and our process and positioning reflect deliberate preparation for the environment ahead.

The Iran conflict has added an urgent dimension to themes we have been building conviction in for over a year: energy infrastructure, real assets, and uncorrelated alternative strategies. We believe the resolution of Middle East tensions, which economic and diplomatic pressure will ultimately produce, could release a powerful tailwind of commodity price normalization, consumer relief and confidence at precisely the moment markets have priced in sustained negative outcomes. Patient, disciplined investors have historically generated their best long-term returns by acting during periods of maximum uncertainty, not after clarity is restored. From a portfolio management standpoint, we favor selective additions to high-conviction ideas, continued emphasis on real assets and alternatives, and disciplined avoidance of areas of the market that do not adequately compensate for risk and liquidity.

Q1 2026 Market Commentary

Equities: Volatile Quarter Amid Geopolitical Uncertainty

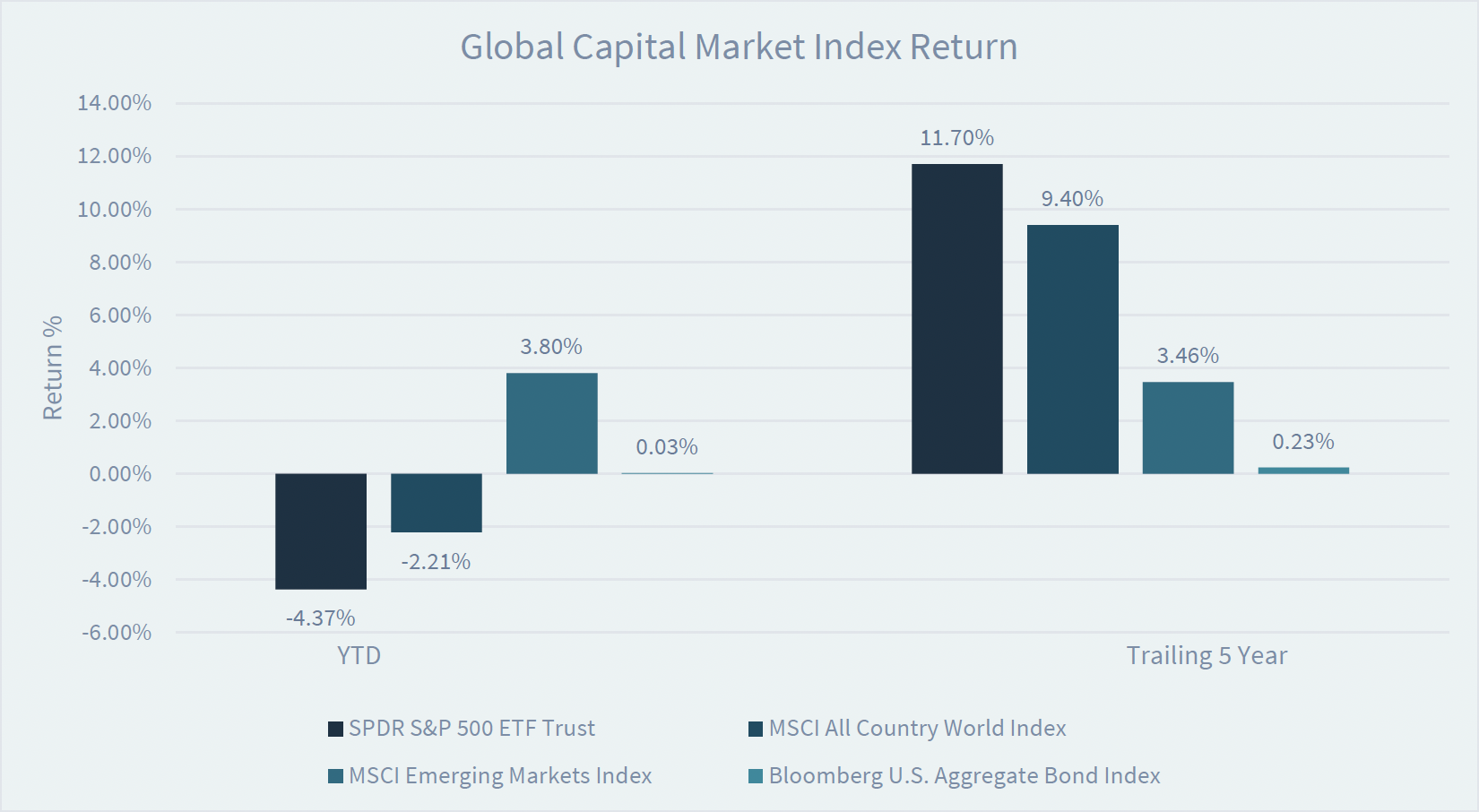

S&P 500: Q1: -4.4%, YTD: -4.4%

Nasdaq Composite: Returns led by AI and semi-conductors: Q1: -7.0%, YTD: -7.0%

Dow: Value outperformed growth significantly; energy sector led all equity sectors: Q1: -3.2%,

YTD: -3.2%

Performance as of 3/31/2026. Source: FactSet

U.S. Equities declined in Q1 2026 following consecutive years of 20%+ gains. The first quarter’s decline was driven primarily by the escalating U.S.-Iran conflict, which sent oil prices above $100. Technology stocks bore the brunt of selling as the Nasdaq entered correction territory, falling over 10% from its January peak. Value meaningfully outperformed growth, and small caps (Russell 2000 +0.9%) held up better than large-cap growth (Russell 1000 Growth -9.8%), confirming a broadening of market leadership.

S&P 500 technology sector earnings grew 22% in FY2025 and are projected to grow 23.7% year-over-year in Q1 2026. The sixth consecutive quarter of double-digit earnings growth. We believe the companies that will generate the most value over the next five years are those that use AI to structurally lower costs, compress development cycles, and defend competitive positions through proprietary data. We continue to favor industry-dominant leaders and invest alongside expert active managers who can distinguish genuine beneficiaries from under discovered opportunities.

Fixed Income: Defensive Yield in Uncertain Terrain

Barclays Aggregate Bond Index: Q1: 0.03%, YTD: 0.03%

Bloomberg Municipal Bond Index: Q1: +0.5%, YTD: +0.5%

Bloomberg Corporate High Yield Bond Index: Q1: -0.8%, YTD: -0.8%

Performance as of 3/31/2026. Source: FactSet

Bond markets were essentially flat in Q1 2026. The 10-year Treasury yield rose approximately 15 basis points to close at 4.32%, as the Iran conflict reignited inflation expectations and reduced the probability of near-term Federal Reserve rate cuts. As of quarter-end, futures markets were pricing zero rate cuts from the Fed in 2026 which is a sharp reversal from expectations of two cuts at year-open.

We continue to favor short-duration assets such as U.S. Treasury Bills and shorter duration High Yield Municipal Bonds, which can offer compelling risk- and tax-adjusted yields while providing a stable anchor in this volatile environment. In general, we do not believe high yield corporate bonds, through public or private debt markets, offer compelling risk/return opportunity given record-low spreads above Treasuries.

When evaluating bonds, we focus on taxable-equivalent (TE) yields to level the playing field across taxable and non-taxable options relative to risk. We believe many areas of the credit market do not adequately compensate investors for the potential risks and illiquidity that could lie ahead. We continue to thoughtfully consider: “Are we being properly compensated for the level of risk taking in the bond markets after tax, and after fees?”

For these important risk management reasons, we prefer U.S. Treasuries and Municipal Bonds for our fixed income and cash management exposure.

Commodities: Precious Metals Continue to Perform

Gold entered 2026 as one of the best-performing assets of the prior year (+60% in 2025) and extended that momentum into January, peaking at approximately $5,417 per ounce. The Iran conflict then triggered a sharp reversal: surging oil prices, a strengthening dollar, and rising bond yields combined to squeeze leveraged gold positions, pulling the metal down to near $4,100/oz in mid-March before a partial recovery. Gold closed the first quarter of 2026 at approximately $4,696/oz — up roughly +4% for the quarter. Structural demand drivers remain firmly intact: central bank reserve diversification, de-dollarization trends, and fiscal debasement concerns continue to underpin the long-term bull case.

Bitcoin: Declined -24.2% in Q1 2026, closing near $65,900, as the risk-off environment driven by the Iran conflict and inflation concerns weighed heavily on digital assets. Despite the price decline, Bitcoin ETFs recorded $2.5 billion in March inflows, ending a four-month outflow streak, signaling that institutional demand remains structurally intact beneath the surface volatility.

Key Data

Source: FactSet

Important Topics

The Iran Conflict and the Energy Shock

The defining event of Q1 2026 was the U.S.-Israeli military campaign against Iran, which began in late February and escalated rapidly through March. The Strait of Hormuz, through which 38% of global seaborne crude and 20% of global LNG transits daily, effectively stalled. WTI crude surged from approximately $57/barrel at year-open to above $102/barrel by quarter-end. Gasoline prices jumped nearly $1.00 per gallon in three weeks. The U.S. economy lost 92,000 jobs in February against expectations of +55,000 gains, and Q4 2025 GDP was revised sharply to +0.7% from +1.7%. The Federal Reserve, already navigating inflation above its 2% target, found itself unable to cut rates without risking further inflation acceleration.

Every major Middle East conflict in modern history has produced sharp short-term dislocations that ultimately gave way to powerful recoveries for patient investors who stayed in quality assets. We view the current environment as consistent with that historical pattern. We are selectively adding to high-conviction positions during this period of maximum uncertainty, consistent with our long-standing belief that the best long-term entry points are found at the intersection of noise and dislocation.

Liquidity Risk in Private Credit

Over the past several years, we have highlighted a key risk that we have observed in private markets: the overallocation to private credit backed by opaque asset values and cash flows, specifically within the data center and software space. While data center growth is highly likely for the foreseeable future, owning a data center that was built 3 years ago is much less valuable than owning a data center that will be built 3 years from now. The rapid expansion of AI hardware and technology (including Orbital Data Centers) creates a risk for the relative value of past data centers due to obsolete technology and the unknown return on investment assumptions for these capital-intensive projects funded through leverage. The uncertainty and fears of illiquidity have driven investors to redeem their capital in excess of what is available causing increasing potential for forced fear selling and/or gated illiquidity.

AI Phase Two: From Infrastructure to Application

Despite near-term valuation pressure on technology names, we believe the AI investment thesis has not peaked but it has entered a new phase. Phase One rewarded the computing substrate: chips, networking, data centers, and cooling. That trade is maturing as supply catches up with demand. Phase Two belongs to the companies that use AI to structurally alter their competitive position. At Cayside, we invested early in chip makers and data center infrastructure. We are now actively building exposure to AI application layer beneficiaries and avoiding those that may be displaced by this new development. We continue to learn from and invest alongside expert active managers who can distinguish the genuine beneficiaries of AI productivity from speculative names. Technology sector earnings are projected to grow 23.7% year-over-year in Q1 2026, confirming that this cycle is broadening into real profit generation, not just capital expenditure. There will likely be winners and losers and the opportunities lie within distinguishing the two.

Energy Renaissance: The Secular and Cyclical Converge

U.S. electricity demand is projected to grow at 8 times the pace of the prior 15 years, driven by AI data center buildout and domestic manufacturing onshoring. Advanced nuclear energy which is reclassified as clean energy under the One Big Beautiful Bill Act (OBBBA) comes with new tax incentives and expanded state financing. We have been building exposure through energy companies with direct earnings leverage to elevated oil prices, and infrastructure companies positioned to power the next generation of AI computing through advanced nuclear, natural gas, and grid modernization.

Business Update & Personnel News

Participation at leading Industry and Investment Conferences continued in Q1 2026, with our team attending leading alternative investment and institutional conferences including hedge fund manager events throughout Florida, Texas and California. These engagements sharpen our manager selection, market intelligence, and overall investment research process — providing direct access to the thinking of the world’s best allocators on behalf of our client families.

Cayside Alternative Fund (“CAF”) — Q1 2026 Update CAF completed its first full quarter in Q1 2026, delivering the uncorrelated performance for which it was designed in a quarter where traditional portfolios faced pressure from multiple directions. Through the end of March 31, 2026 the fund is estimated up +2.5% year to date while the S&P500 was down -4.4%. We are expanding the roster of underlying managers in Q2 2026 and will distribute a dedicated CAF quarterly update to participating families. For families not yet participating, CAF provides access to institutional-quality alternative investment managers at substantially reduced minimums, with improved custody and oversight.

Michael Rhea Joins Cayside as Director, Portfolio Manager & Client Advisory On April 1, 2026, Mike Rhea officially joined Cayside Partners as Director, Portfolio Manager & Client Advisory. Mike brings extensive experience in portfolio management, investment research, and client advisory across institutional and high-net-worth families. His addition strengthens our team’s depth and capacity to deliver best-in-class investment solutions and personalized service to our growing client base. Welcome, Mike.

Cayside Partners Recognized on the 2026 Seminole 100 Cayside Partners was named to the 2026 Seminole 100, which recognizes the fastest-growing businesses owned or led by Florida State University alumni. Cayside Partners was ranked 10th and was honored at the ninth annual Seminole 100 celebration on February 21, 2026 at the Donald L. Tucker Civic Center in Tallahassee. This recognition reflects the trust our clients place in us and the dedication of our entire team.

We appreciate your support and confidence in our process and are excited to keep adding value for each of our client families.

Disclosures: Cayside Partners, LLC ("Cayside") makes no warranty as to the accuracy or completeness of any data herein. Information presented in this report is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. Investments involve risk and are not guaranteed. Past performance is not indicative of future results. This report is intended for the recipient(s) only and not for further distribution without written consent. Investment advice offered through Cayside Partners, LLC, a Securities and Exchange Commission registered investment advisor able to provide investment advice in states where it is registered, exempt, or excluded from registration. Content contained herein should not be construed as an offer or solicitation for investment advice or for the purchase or sale of any security, insurance, or other investment product. Investments involve the risk of loss, including possible loss of principal. Please consult with a qualified financial, tax, accounting, or legal professional before implementing any ideas or strategies discussed here. Content provided is obtained from sources believed to be reliable but cannot be guaranteed as to its accuracy or completeness. The AUM figures disclosed herein are as of March 31st, 2026, and may be subject to change. Our firm's AUM figures are reported on a gross U.S. Dollar basis and may include assets managed on a discretionary and non-discretionary basis. Past performance is not indicative of future results, and AUM figures are subject to change. For further information regarding our firm's AUM or to obtain a copy of our most recent Form ADV, please contact us.