Cayside Review: 2026 Q2

This newsletter includes our 2026 Second Quarter review, global market update and outlook, key numbers, and announcements.

“First of all, never play macho man with the market, second of all, don’t overtrade.”

-Paul Tudor Jones

The first half of 2026 was marked by renewed conflict in the Middle East, an oil supply shock and a drawdown in equities markets. In June, geopolitical tensions de-escalated and energy prices normalized causing U.S. equity indices to recover losses and reach record closing highs. Despite the volatility and fear, the disciplined investor was rewarded with a powerful recovery. The round trip in prices reaffirmed a lesson we return to often: the best long-term entry points are found at the intersection of noise and dislocation. Our deliberate positioning in high quality equities, fixed income, and uncorrelated alternative strategies served client portfolios well through both the decline and the rebound.

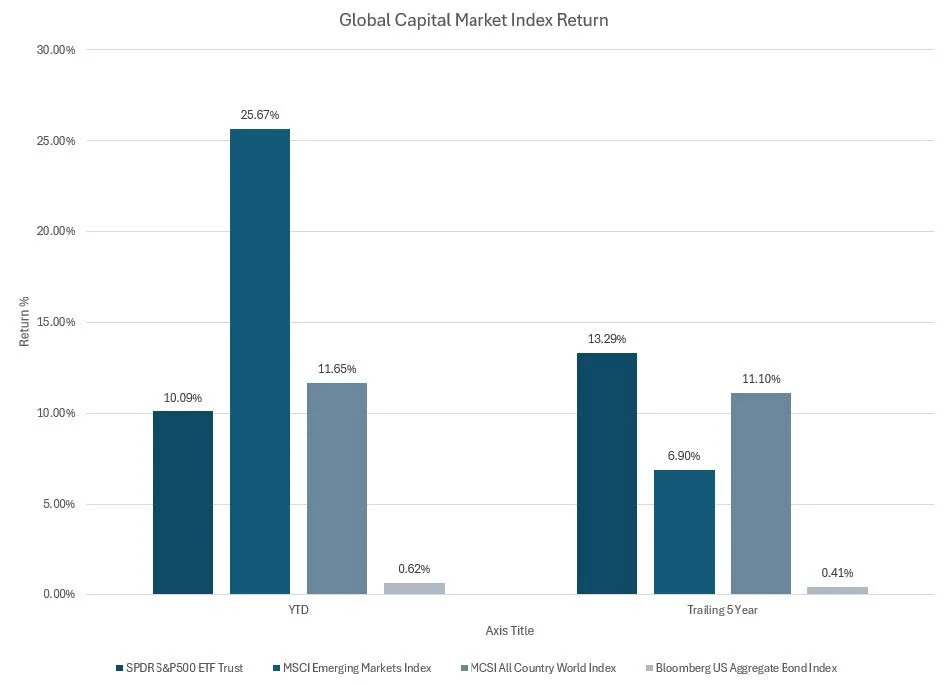

The S&P 500 returned 15.20% for the quarter and 10.21% for the year, as several companies in the “Magnificent Seven” were revalued downward by the market and leadership rotated away from Software Services and toward AI and semiconductors. Corporate earnings delivered another quarter of double-digit growth and net margins are among all-time highs.

With major indices reaching new peaks, our focus is to remain disciplined at elevated valuations while continuing to search for opportunities in overlooked areas of dislocation. We continue to favor selective additions to high-conviction ideas, a durable emphasis on real assets and alternatives, and disciplined avoidance of areas of the market that do not adequately compensate for risk. Periods of optimism should be matched with thoughtful risk management to protect long-term value and compounding of client capital.

Q2 2026 Market Commentary

Performance as of 6/30/2026. Source: FactSet

US Equities:

S&P 500: Q2: 15.20%, YTD: 10.21%

Nasdaq Composite: Q2: 21.60%, YTD: 13.13%

Dow: Q2: 12.90%, YTD: 8.86%

Equities: A Powerful Recovery to Record Highs

Despite multiple global conflicts, oil price shocks and consistent fear over valuations this year, the quality of earnings growth warrants a cautiously optimistic approach. S&P 500 earnings are set to grow roughly 25% year-over-year on 12% revenue growth. While these figures are optimistic, without AI infrastructure and energy, the rest of the S&P500 is growing earnings at a more modest 8%.

S&P500 and Nasdaq have increasingly become concentrated in technology companies. The ten largest companies are roughly 40% of the S&P 500, and the “Magnificent Seven” alone are about a third of its market value. Many investors believe they are adequately diversifying portfolios by owning index funds, however we believe high concentration and creative destruction due to advances in technology make this thesis increasingly fragile.

The volatility and rotation in the first half of 2026 was a living preview of how quickly concentration can cut both ways. AI infrastructure is propping up both index earnings and a sizeable portion of US GDP and single disappointment from AI capital-spending guidance could compress estimates broadly. We remain focused on the risk around future concentration unwinds and/or AI capex disappointment. For these reasons, we favor broad equity exposure and diversification in areas such as dividend growth, quality, and mid/small-cap companies.

Fixed Income:

Barclays Aggregate Bond Index: Q2: 0.67%, YTD: 0.62%

Bloomberg Municipal Bond Index: Q2: 2.50%, YTD: 2.32%

Bloomberg Corporate High Yield Bond Index: Q2: 2.66%, YTD: 1.68%

Performance as of 6/30/2026. Source: FactSet

Fixed Income: Defensive Yield in Uncertain Terrain

We prefer high-quality, liquid sectors over riskier, potentially illiquid credits, where tight spreads offer inadequate compensation amid normalizing fundamentals, elevated supply, and issuer dispersion. U.S. Treasuries stand out for their compelling liquidity, while municipal bonds have become particularly attractive after a Q1 repricing, with taxable-equivalent yields at favorable levels relative to the fixed income complex. Municipal Bonds provide superior risk-reward, tax efficiency for higher-bracket investors, and resilience in an uncertain macro backdrop of fiscal pressures and cautious Fed policy. This positioning delivers reliable income, portfolio ballast, and downside protection while avoiding overexposure to credits vulnerable to economic softening and potential for illiquidity

Alternatives: Continue to Outperform

We continue to favor real assets and alternatives and have allocated deliberately within portfolios when appropriate. Given the elevated risk of geopolitical and inflation uncertainty, precious metals and commodity exposures remain attractive. In addition, the equity and technology environment is likely to continue to show opportunities for alternative strategies and domain experts in investable areas of technology.

Important Topics

Space Launch and Communication Companies

The space sector has entered a transformative phase in 2026, propelled by rapid advancements in reusable launch technology and the explosive growth of satellite constellations. The industry continues to advance by cutting launch costs and enabling satellites to provide communications to millions of subscribers (and growing) globally.

The ripple effects of drastically reduced launch costs lower capital intensity for every downstream space business and direct-to-smartphone service. We expect multiple compression in legacy telecom and tailwinds for launch suppliers and new industrial application in defense, communications and logistics, among others.

Creative Destruction from AI on Existing Businesses

AI is accelerating creative destruction across the economy, dismantling legacy business models while birthing more efficient alternatives. Software, media, professional services, and knowledge-work sectors face intense pressure as generative tools automate routine tasks, compress margins for mid-tier players, and shift value toward AI-native platforms. Over $1 trillion of enterprise software market cap was erased in the first half of 2026, dubbed, the "SaaSpocalypse."

This disruption drives productivity gains and GDP support through capital investment, but creates short-term labor market frictions and corporate winners and losers. Investors must prioritize adaptable companies embracing AI integration while laggards risk obsolescence. We believe, the net effect is profoundly positive for growth and innovation, rewarding agile capital allocators who navigate the transition properly. Destruction funds creation and as productivity accrues to adopters, the investment environment is primed for opportunity and risk.

Illiquidity Concerns in Private Markets and Upcoming Mega-IPOs

As we have written in past letters, private credit and private equity markets face mounting illiquidity as extended hold periods, optimistic valuation marks, and capital return pressures collide with surging demand for liquidity from landmark IPOs. Private credit's expansion, largely financing AI infrastructure, introduces opacity and mismatch risks in a higher-rate environment, while Private Equity funds grapple with delayed exits and potential markdowns.

The anticipated IPO wave in 2026 promises massive liquidity events but risks the potential for a market vacuum as capital is reallocated from existing public holdings, and post-lockup selling pressure at elevated valuations. These dynamics underscore the premium on true liquidity in portfolios. We favor selective exposure to these transformative names via public channels where possible, while cautioning against over-reliance on private marks that may not withstand scrutiny amid normalization. This shift enhances overall market transparency but highlights the need for disciplined risk management in alternatives.

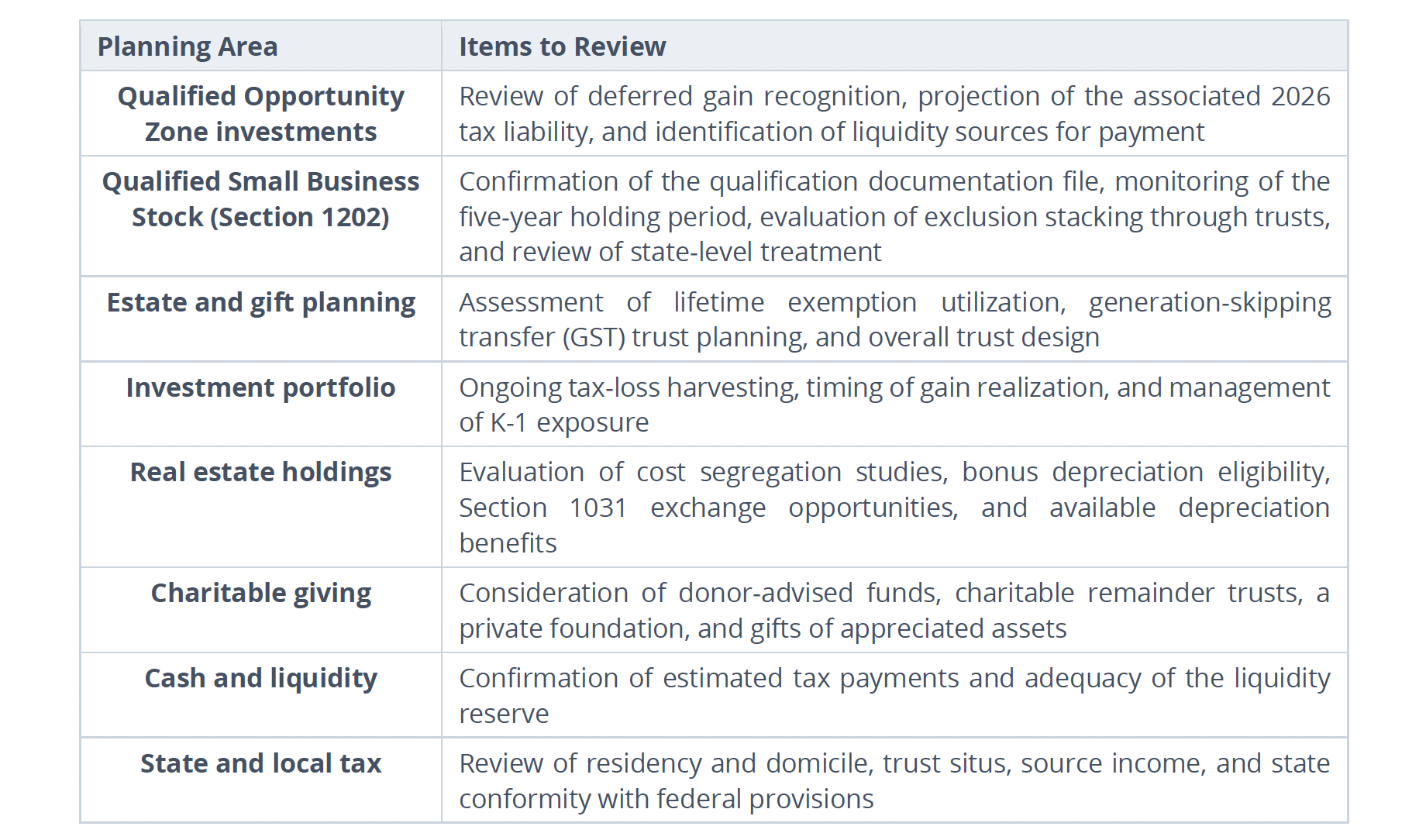

Mid-Year Planning Priorities for Family Offices

The midpoint of the year is an ideal time to revisit the planning items that compound quietly over time. Heading into the second half of 2026, we are proactively reviewing several priorities with our client families: tax harvesting losses and managing gains around concentrated and appreciated positions; revisiting estate and gifting strategy while the elevated lifetime exemption remains in place; evaluating Roth conversion windows; and stress-testing liquidity for capital calls, tax payments, and near-term goals. We are also conducting concentration-risk reviews for families with large single-stock or pre-IPO exposure, where hedging, diversification, and charitable strategies such as donor-advised funds can reduce risk in a tax-aware manner.

Qualified Opportunity Funds (QOFs)

For families who rolled capital gains into Qualified Opportunity Funds, the original deferred gain generally becomes taxable on the earlier of a sale/exchange or December 31, 2026. That means many families will have a tax bill even if they still own the QOF investment and have not received liquidity. The IRS confirms that QOF deferral lasts only until the earlier of sale/exchange or December 31, 2026. This is a significant item for families who participated in QOF Funds to keep in mind and could also be an event to monitor in market liquidity.

After a strong recovery in equity markets, these reviews are especially timely. If any of these topics are relevant to your situation, we welcome the conversation.

Business Update & Personnel News

Participation at leading Industry and Investment Conferences continued in the second quarter of 2026. Our investment team attended leading alternative investment and institutional conferences, and our Chief Investment Officer completed a research trip through Switzerland and London focused on European family office governance, the persistent U.S. versus international valuation gap, and emerging technology themes. These engagements sharpen our manager selection, market intelligence, and overall research process, providing direct access to the thinking of the world’s best allocators on behalf of our client families.

Cayside Alternative Fund (“CAF”) — Q2 2026 Update Through the second quarter of 2026, CAF continued to deliver the differentiated, lower-correlation profile for which it was designed, and is estimated to be up approximately 23% year to date through June 30, 2026.1 We expanded the roster of underlying managers during the quarter and will distribute a dedicated CAF quarterly update to participating families. For families not yet participating, CAF provides access to institutional-quality alternative investment managers at substantially reduced minimums, with improved custody and oversight.

Welcoming Danny Green, Summer Analyst Intern We are pleased to welcome Danny Green to the Cayside team for the summer. Danny is a rising junior at the University of Florida studying Finance with a minor in Philosophy, Politics, Economics, and Law. He brings a genuine passion for investing and a deep curiosity about the stock market, real estate, and how markets and economies move. Danny is supporting our investment research and next generation education curriculum efforts this summer, and we are glad to have him.

Celebrating a New Arrival Congratulations to Mike Rhea, our Director of Portfolio Management, and his family on the arrival of their daughter, Elle, born May 27, 2026. The entire Cayside family could not be happier for the Rheas. Welcome to the world, Elle.

Firm Growth & Milestones Cayside continues to grow alongside the families we serve. We are currently managing, advising and reporting on +$580MM as of June 30, 2026.2 Additionally, we have added more resources and strategic partners for Family Office Services and building out a true multi-family office. We remain grateful for the trust that makes this growth possible.

We appreciate your support and confidence in our process and are excited to keep adding value for each of our client families.

1 Performance figures for the Cayside Alternative Fund are preliminary estimated and are unaudited. They are based on performance for the underlying managers as provided to us by third parties, including fund administrators and the managers themselves. These estimates have not been independently audited verified by Cayside and are subject to revision once final figures are received. Actual results may differ, and the figures shown may not reflect the return of any individual investor’s position after fees expenses. Past performance is not a guarantee of future results.

2 The figure shown reflects assets that Cayside manages, advises on, and reports on as of June 30, 2026, and includes categories beyond regulatory assets under management. It may include assets held away, assets for which we provide advisory or reporting services only, and assets managed by third parties, and it is not equivalent to the regulatory assets under management reported in our Form ADV. The figure is unaudited and is calculated using account values data as of the date shown.

Disclosures: Cayside Partners, LLC ("Cayside") makes no warranty as to the accuracy or completeness of any data herein. Information presented in this report is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. Investments involve risk and are not guaranteed. Past performance is not indicative of future results. This report is intended for the recipient(s) only and not for further distribution without written consent. Investment advice offered through Cayside Partners, LLC, a Securities and Exchange Commission registered investment advisor able to provide investment advice in states where it is registered, exempt, or excluded from registration. Content contained herein should not be construed as an offer or solicitation for investment advice or for the purchase or sale of any security, insurance, or other investment product. Investments involve the risk of loss, including possible loss of principal. Please consult with a qualified financial, tax, accounting, or legal professional before implementing any ideas or strategies discussed here. Content provided is obtained from sources believed to be reliable but cannot be guaranteed as to its accuracy or completeness. The AUM figures disclosed herein are as of March 31st, 2026, and may be subject to change. Our firm's AUM figures are reported on a gross U.S. Dollar basis and may include assets managed on a discretionary and non-discretionary basis. Past performance is not indicative of future results, and AUM figures are subject to change. For further information regarding our firm's AUM or to obtain a copy of our most recent Form ADV, please contact us.